Wavestone recently attended the Global Sourcing Association’s Public Sector Day 2017 that focused on the latest developments in public sector digital transformation. It also emphasised the importance of strategic sourcing at a time when public services face great pressure to deliver affordable services that satisfy an increasingly digitally connected audience.

The varied and enthusiastically delivered agenda brought together representatives from central government departments, senior public sector procurement analysts and SMEs in disruptive technologies such as RPA (Robotics Process Automation).

Capturing the curiosity of the room due its disruptive capability and mysteriousness was blockchain – a potent platform which has the potential to significantly influence the development of digital public services.

What is blockchain?

Blockchain is a distributed general ledger shared across a network of multiple sites which is a new way to record and verify data and transactions, creating an immutable record of all the transactions in the network. When a transaction occurs, special individuals, known as ‘miners’, compete to verify them. The first individual that can successfully confirm the transaction is correct receives a reward (X units of bitcoin – or other digital currency). Bitcoin is a digital currency which resides in an individual’s digital wallet.

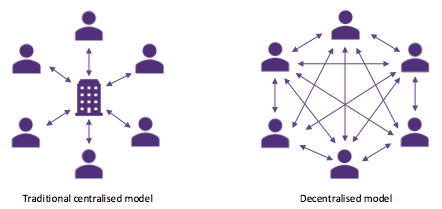

The concept of blockchain has certainly gathered momentum in the wider sector, not least due to two key papers: (i) Innovations in payment technologies and the emergence of digital currencies (BoE: 2014) and (ii) Distributed Ledger Technology: beyond blockchain (Government Office for Science: 2016). These documents not only represented interest in blockchain by central government organisations but also recognised a distinction between our traditional centralised infrastructures, in which we all retain our own records with overlapping transaction sets, to a distributed synchronised network of records whereby all parties have the exact same copy of the transaction set which has been 100% validated by the parties.

What does blockchain mean for the Public Sector?

Blockchain provides several potential use cases:

Data sharing and security in high transaction volume environments

- In the NHS or HMRC for example, blockchain could be used to grant the individual, access to their data and give them the right to disclose and own that data, which will significantly reduce the overhead of multiple sharing of multiple records.

Budget management

- Given that the store of value is electronic and it resides in a digital wallet, it is possible to be very selective in the way spend is allocated. For example, for NHS spend, we want to direct 9.8% to social care; recipients of that, then receive a digital wallet which only allows them to receive that set amount of money and spend it in a set time.

- In another example, the Papua New Guinea Central Bank is looking to implement this concept in the funding for farmers by using a digital wallet to allocate exactly how much they can spend on only seed, gasoline and agricultural tools.

Smart contracts

- Blockchain will allow electronic measurement of the supplier performance. Buyers will no longer need to refer back to a large contract document because all of the contract data will be captured and will simultaneously be used as a reference point to confirm either yes/no goods were delivered and yes/no value was exchanged.

In our view, there are some substantial benefits of blockchain’s decentralised model with its potential to rationalise central government processes, invoke more efficient data sharing and improve the transaction process (through budget control and the ability to overlay contractual framework).

Crucially, however, it will not be the technology itself which determines its success, but rather the willingness of users to embrace change and the impact it has on current systems. For example, the implementation of Digital (read: blockchain-based) Wallets for benefit payments at the Department of Work and Pensions was impeded not because of the shortcomings of the technology, but because consumers were uneasy about the control it gave the authorities over what recipients could use the money for.

One further key point to highlight is the uncertainty around blockchain technology due to the lack of formal regulation. This brings risk for public services and as a result, it will only be implemented once proven as commercially viable, safe, regulated and reliable.

Blockchain is certainly a large jump forward from the status quo of transacting. It is on the digital horizon, but lacking a regulatory framework and not having even been fully trialled by the private sector yet, it may be some time before we see its full implementation into the public sector.

Related Insights