Clarification of different models and trends

With the ground breaking arrival of low-budget airline, French Blue, on Paris (Orly) – Punta Cana flights and the increased number of offers in the Long-Haul Low-Cost (LHLC) carrier segment (notably Eurowings which offers bargain-basement prices on flights from Cologne to Dubai, Cuba and Bangkok), the question of LHLC carriers is again at the forefront of airline sector news, especially after the announcement of Air France’s strategic plan, Trust Together.

The LHLC formula draws on the same ingredients that made the traditional low-cost model a success and adapts these to take account of the specific constraints of long-haul carriers; a strategy that certainly seems to be paying of for several players, such as Air Asia X and Norwegian Air Shuttle. Despite the implications of the generic “low-cost” term, the LHLC model is by no means fixed low-cost concept. indeed, significant changes taking place in this segment are considerably modifying the original low budget model. An in-depth analysis of these trends indicates a global reshaping of the airline landscape and the harmonization of offers. A new trend is emerging, focused on different customer experience concepts, with personalized services, a more or less flexible offering and perceived value that ranges from the quest for “status”, proposed by the longstanding sector leaders, and the «good deal» implied by the low-cost model.

Adapting the low-cost model to long-haul carriers

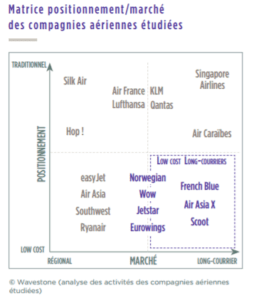

As illustrated below, several players have ventured into the LHLC segment and are beginning to produce promising results, even though adapting the low-cost value proposition for long-haul carriers gives rise to a number of questions. To underline the respective positioning of the airline companies under review from a comparative perspective, the following graph shows the positioning of certain airlines relative to two axes: the market for airline companies in the short to long carrier segments and their positioning by service offered:

Can the low-cost model simply be transposed to long-haul carriers?

The LHLC model is based on the ive key factors that have underpinned the success of low-cost carriers, and which have enabled them to capture an increasing share of the market and generate high returns. For example, the operating margins of ryanair, airasia and southwest airlines were two to three times higher than the sector average in 2014. The rigorous implementation of these levers has caused a radical reshuling in the airline market for short and mediumhaul carriers, especially since the trend in attractive air fares has triggered latent demand for short trips in europe.

Expansion of certain LHLC companies

While the medium-haul low-cost carrier segment has expanded by offering cheaper fares than traditional airline companies, this price differential is considerably more difficult to achieve on long-haul carriers given their specific constraints. Despite these difficulties, some airlines are generating promising operating and financial results. This has given rise to four Long-haul Low-Cost company models. While all of these models are underpinned by the same fundamentals, they do not necessarily benefit from the same advantages in the ongoing market reshule, notably vis-à-vis the sector majors.

Against this backdrop, Air France has launched a newCo spin-off (a separate entity as yet unnamed). This parallel company, whose offer is relatively less expensive than that of its parent without being low-cost, is targeting a different category of clientele and is envisaged as an innovation laboratory for the group.

An ever-evolving business model

Since its launch, the low-cost model has undergone several changes that are now being adopted by the diferent long-haul low-cost models.

Steady shift towards major airports and other hubs

While the first low-cost models tended to operate through secondary airports for financial reasons, recent trends show that more and more players are refocusing on major airports, particularly since LHLC airlines have to ill higher capacity planes. This could see the emergence of a new type of hub allowing medium-haul low cost carriers to feed low-cost long haul lights; a trend which could have an impact on current airport models in terms of airline assignment, baggage handling and light connecting paths, etc. In this context, the Daughter model and, to a lesser extent, the pure model stand to benefit from the fact that they can draw on the alliances, network and hub of their parent company to optimize occupation rates.

Diferentiation and additional services and options

Additional paying options are key to the low-cost business model. For example, these options account for 25% of Ryanair’s revenues (~ €15 on average per passenger in 2015)2 , and 15% of those of Norwegian air shuttle . Long haul low-cost carriers are boosting this major growth driver by differentiating their offerings:

/ Desiccation of economy class seats, which, when combined with premium-class services, generate additional revenues (e.g. French blue offers upgraded services on 28 of the 378 passenger seats in its a330-300)

/ Low cost Daughter airlines enhance their brand appeal, either by using the loyalty programs of their parent company (e.g. Jetstar/Qantas Frequent Flyers, air asia X/Big of air asia), or by developing their own (e.g. Westjet rewards). Likewise, the shift towards major airports could also benefit players who can rely on parent-company backing.

Forging alliances

In an increasingly competitive environment, traditional airline companies began forging alliances in the 1990s in a bid to offer their customers access to a more extensive network and to optimize occupancy rates in large capacity planes. The major alliances, such as star alliance, oneWorld and skyteam, are vying fiercely to ofer customers the most advantageous loyalty programs possible with regard to flight miles and services. in terms of competitive edge, low-budget airlines benefit from a different kind of advantage in that they did not invest in alliances or costly loyalty programs at the outset. however, the reshuffling of the airline landscape could now incite them to do so. as such, 2016 saw the emergence of two low-cost alliances in asia; U-FLY, in January, comprising hong Kong express, Lucky air, Urumqi air and West air, and notably, Value alliance partnership in May, which mainly covers low-cost subsidiaries of major asian airlines, as illustrated in the chart opposite (igure 1). as such, low budget airlines are also trying to cash in on network complementarity and code sharing in a bid to enhance their geographic coverage and optimize occupancy rates.

Heading for the best of both worlds : from modelhybridization to customerexperience segmentation

Emergence of low-cost hybrid models: budget airlines taking on legacy-carrier proile and legacy carriers ofering low-cost models

The development of hybrid models is now under way: as illustrated in igure 2 above, low-budget airlines are beginning to adopt a legacy-carrier proile and legacy carriers are now ofering low-cost models. this trend, already apparent in the lowcost medium-haul segment, is paving the way for sector reshaping in several key areas:

- Increased eforts of traditional airlines to achieve operational eiciency, an issue which takes on greater importance when oil prices rise. these players model their eiciency optimization strategies on low-cost methods

- Low-cost airlines ofering personalized services fall into the «value carrier» category. given the subtle segmentation of services, this ofer difers from the pure low-cost model in that it proposes customized services and, in some instances, loyalty programs.

- a new premium access segment proposed by independent players, such as La Compagnie and low-cost airlines including JetBlue (with its Mint Class ofering) and Frenchblue (premium Class).

- the development of air routes to airport hubs and the creation of alliances

- Dynamic trends in sector consolidation and partnership agreements could further blur the dividing lines between low-cost (short, medium and long-haul) and legacy models, and allow airlines exposure to all segments (leisure/business/VFr4 ). this convergence of offers could lead to the convergence of prices for equivalent services in the medium term, a trend which has more or less been triggered by the wide-spread practices of Yield Management and the virtually real-time adjustment of prices to demand and competitive trends. For example, when confronted with the aggressive tariff policy of French Blue on lights to punta Cana, air France immediately came back with a counter proposition: in this case, the issue is how long these players will be able to hold out without causing any longterm margin deterioration.

The customer-experience: a diferentiating factor

The act of purchasing has always involved a psychological process speciic to each individual; some may seek the fairest price while others prioritize service or company status. As such, beyond the convergence of models and prices, companies can tap into the signiicant potential arising from the differentiation of their products or services by adopting a more personalized, client-centered approach based on customer perception and experience. Given the digitalization of cities, airports and other travel-related venues, we believe that the services linked to digital behavior patterns will rapidly become commodities and that digital amenities, such as onboard WiFi access, should be included in the basic packages ofered by airline companies. The current dividing lines between airline services oferings will thus be modiied and the overall challenge for companies will lie in their ability to capitalize on digitalization to ofer new, paying services (inlight retail, inlight entertainment) as a means to ofset the reduction in air fares and inance investments made. The ability of a company to create a veritable brand environment that meets the diverse expectations of its customers is also key to corporate expansion: while travelers seeking eiciency can choose a standard, simple and smooth passenger light, those looking for a more memorable trip, can opt for personalized and innovative services. This certainly augurs well for the air-travel business and provides a tremendous opportunity for airlines to come up with new dream themes for travelers !

Related Insights