The ABC / ABM model (Activity Based Costing / Activity Based Management) has gained increasing popularity in recent years. Numerous information system divisions use the model to calculate the cost price of services rendered and align their price lists accordingly. Yet, the model needs to be refocused on its primary function: performance management.

Using ABC / ABM not just to calculate costs but to manage performance

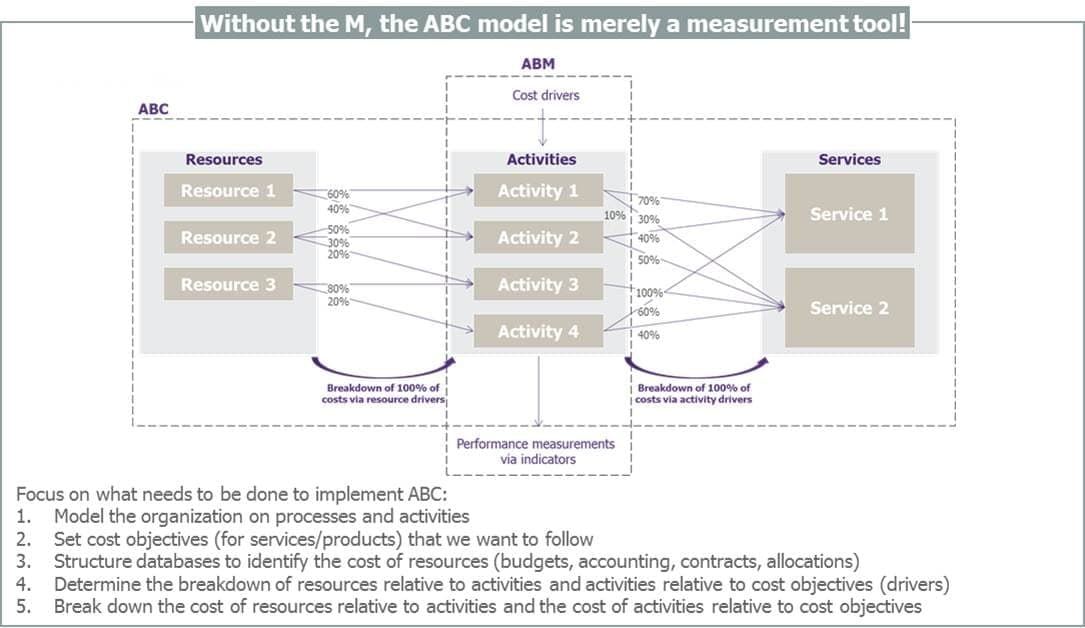

To provide services to users, all IS divisions use resources (such as labor, outsourced services, and IT infrastructures) through activities (processes). To obtain and use these resources effectively and efficiently with a view to meeting objectives, more and more IS divisions are adopting an activity-based management system: the ABC / ABM model.

- ABC is a method used to make connections between the resources consumed, activities used and services produced by a company. The aim is to faithfully reflect the economic reality of an organization and in particular to precisely measure cost prices.

- ABM is focused on managing activities so as to improve the performance and optimize the profitability of the entity in question. The idea is to use the cost modeling generated by the ABC method to measure performance and guide managerial decisions.

To summarize, ABC is used to understand the formation of costs and the factors that impact those costs, while ABM is used to modify costs so as to optimize operations. In short, ABC addresses the question, “How much does it cost?”, while ABM responds to the question of “Why does it cost that much?”, this last query being vital to any continuous improvement approach.

Boosting performance with ABC / ABM

The key strength of the ABC / ABM model is that it can be used to observe IS divisions through the prism of their activities (i.e. their organization systems and processes), thereby serving to combine visions with often conflicting interests:

- An economic vision, aimed at optimizing expenditure and increasing company revenues;

- An operational vision, seeking to improve quality and accelerate the production of services;

- A strategic vision, which seeks to adopt a forward-thinking approach, anticipating market and competitor trends.

The results obtained using the ABC / ABM model help to unify the IS division’s various stakeholders by providing a cross-functional vision for each business activity. The model serves to break down walls between IS functions by making it possible to set shared objectives and providing the tools for monitoring those objectives.

There is no standard user guide for the ABC / ABM model, quite simply because the environment and strategies of IS divisions are numerous and varied, as are the personalities of their CIOs. The activities for which management performance is prioritized – and for which relevant objectives are set – inevitably vary from one IS division to the next.

ABM involves making different uses of the information provided by the ABC model, such as :

- Value analysis: identifying business activities that contribute to the creation of value and improving them. Activities that fail to add value should be limited in order to reduce costs without affecting value for customers, business lines, and users.

- Analysis of profitability / cost reduction: studying the future impacts on costs and profitability of a change in organization (acquisition, outsourcing, etc.). The goal with this type of analysis is to compare “before” and “after” situations (for example, following the outsourcing of an activity or a decline in service level).

- Benchmarking: comparing IT organization systems (internal or external) to take away the best practices in a given area while remaining aware of the limits of these sources of inspiration, with each organization having its own specific characteristics.

- Productivity analysis: identifying the time needed to complete the same task or provide the same service. The objective here is to detect areas of non-performance with a view to rolling out optimization initiatives.

Rome wasn’t built in a day, and the same holds for managing company performance through the ABC/ABM model. To obtain reliable results and integrate this management system in the company culture, IS divisions need to begin by implementing the model while deploying the necessary resources, such as skills and tools.

A complex model requiring the talents of a pluridisciplinary team

The implementation and long-term use of the ABC/ABM model calls for a dedicated team fully aware of the issues involved in the management of economic performance. The IS division has to work closely with management control and model experts, both in building and revising the system, to ensure its reliability (the division of activities, services, drivers, etc.) and, most importantly, the dissemination of a management culture throughout the IS division.

A number of professional organizations specialized in information systems or management control share their take on the model as well as standard guidelines (activities, drivers), enabling companies to make a comparative analysis of their IS costs. These guidelines may serve as sources of inspiration, but the specifics of each IS division are such that they have to be adapted before implementation (for example, by changing the activity guidelines or by replacing a driver by an “expert measure”). The guidelines also need to be adjusted to the maturity of the IS division and the economic challenges to be coordinated, as well as feasibility constraints.

Consequently, the key challenge for IS teams lies in matching the granularity of the model with the maturity of their department (in financial, technical and organizational terms). That balance struck, companies implementing the model are rewarded by the possibility of using the ABM model to manage costs, contributing to the objectives of IS divisions and their various units.

In conclusion, ABC / ABM provides IS divisions with the keys to high-value-added performance management. The transformation calls for several specific prerequisites. The availability of data (on budgets, inventory, etc.) for fueling the model is absolutely vital. The ABC/ABM approach requires the active contribution of all employees at all levels of the company. It is also important that companies set realistic objectives relative to the benefits of the model and its level of detail. And lastly, the reliability and relevance of the model will rely to a great extent on the degree of maturity of the IS division and the proven nature of the construction hypotheses of the model.

Related Insights